Executive Signaling and the Escalation Ladder

Signal Compression and Market Detection Lag

Markets appear surprised that volatility did not accelerate more quickly following the latest developments between the United States and Iran.

Much of that reaction assumes escalation still follows the traditional geopolitical playbook: weeks of signaling, visible diplomatic breakdowns, legal framing, and coalition positioning. When those signals unfold gradually, the escalation pathway is legible, giving markets time to interpret and price geopolitical risk.

In strategic terms, markets often react to signals along what security scholars describe as the “escalation ladder”—the structured sequence of diplomatic, political, and military steps through which conflict typically intensifies, a concept associated with Herman Kahn. Closely related is the role of strategic signaling by political leaders, which shapes how adversaries and observers interpret intent and resolve, a dynamic explored by Thomas Schelling and later formalized in crisis signaling theory.

In this case, however, the sequence appears to have been far more compressed.

This dynamic can be understood as signal compression in conflict escalation—the shortening or bypassing of the traditional signaling stages through which conflicts typically escalate, thereby reducing the time available for institutions and markets to interpret risk.

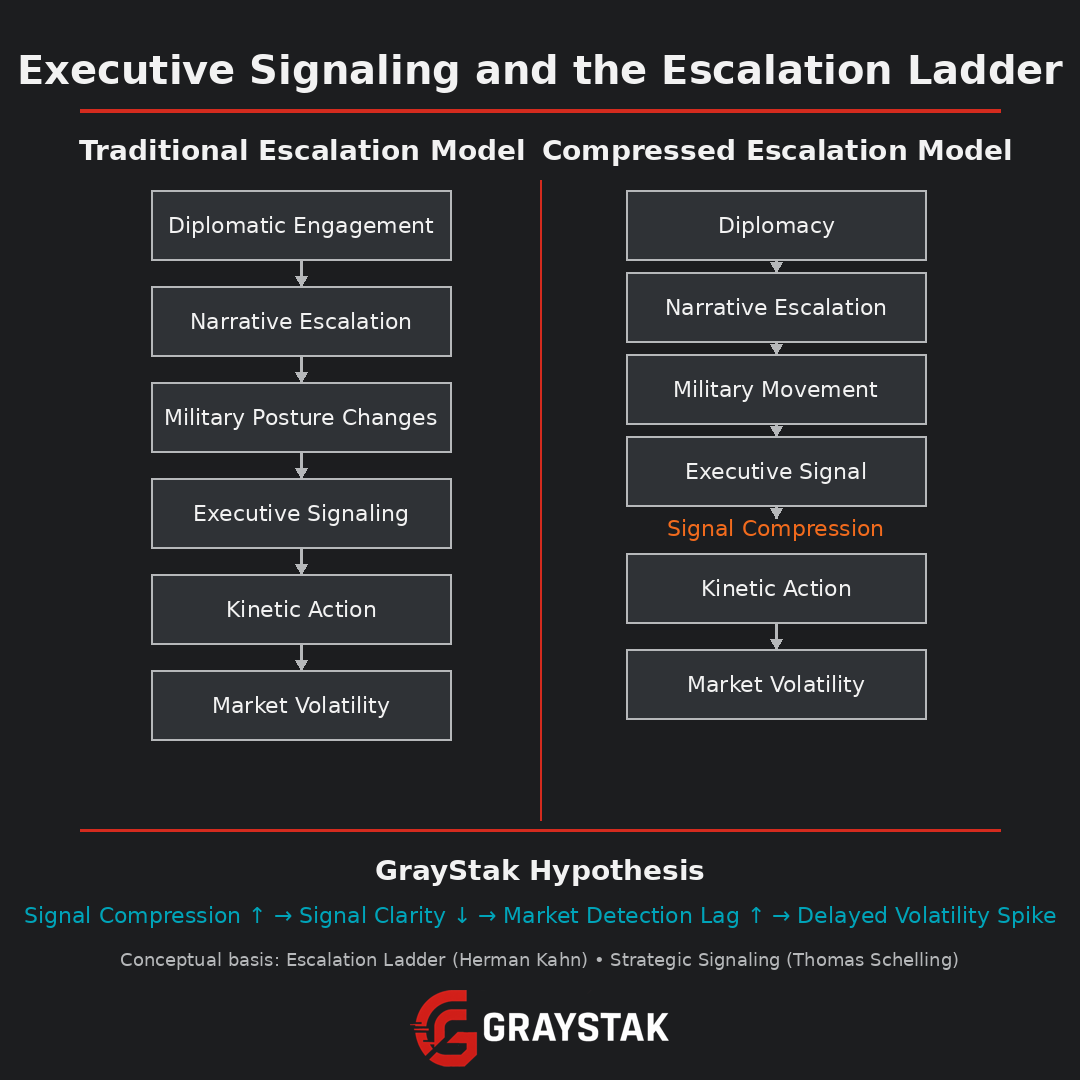

Figure 1 — Traditional escalation pathways versus compressed escalation signaling

As illustrated in Figure 1, escalation signals can collapse into a compressed sequence.

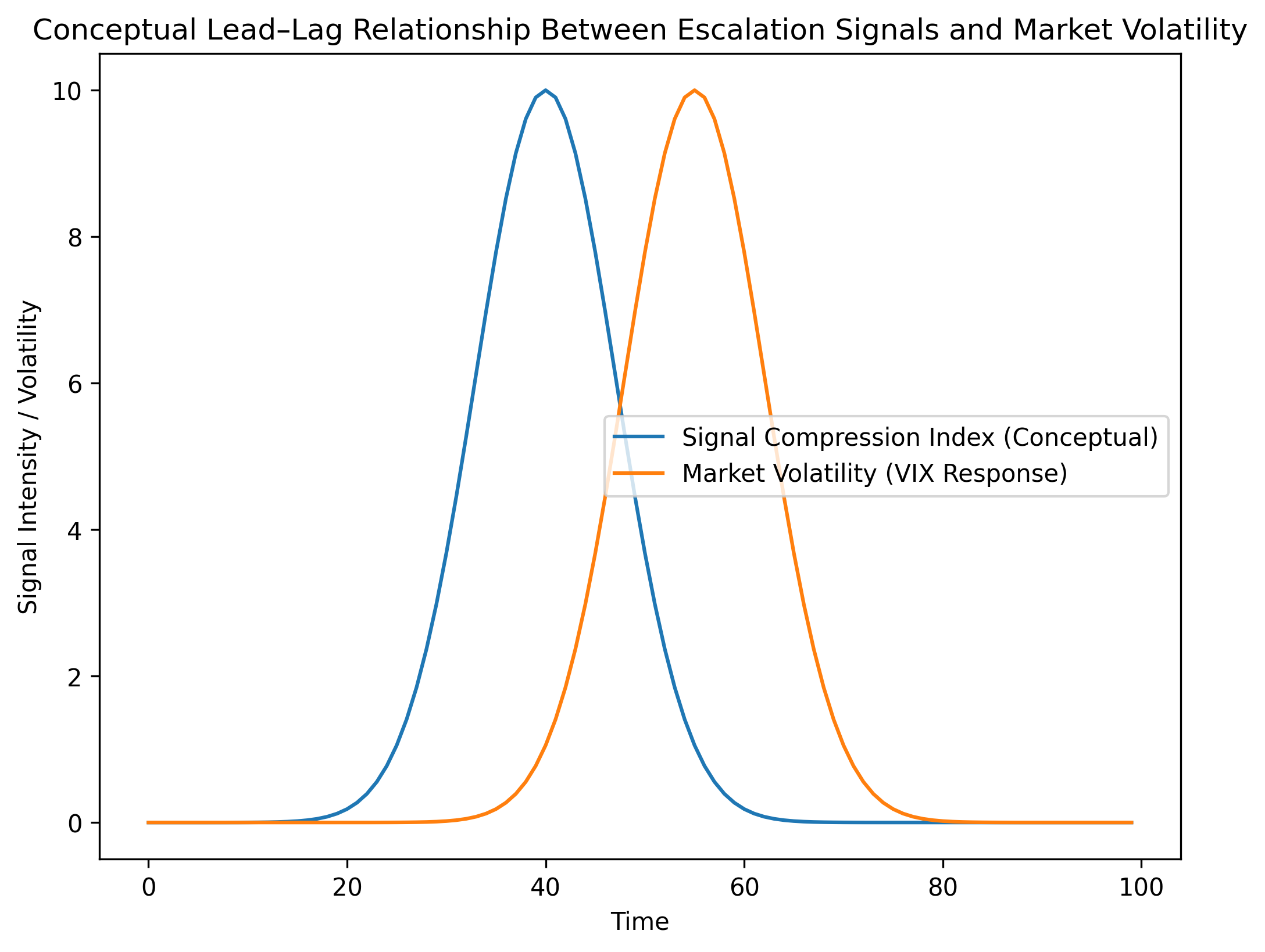

When escalation signals compress in this way, the lag between geopolitical events and market volatility can widen because the informational cues markets typically rely on to detect risk appear later—or not at all. As illustrated in Figure 2, compressed escalation signals can precede volatility spikes, creating a measurable lag between geopolitical developments and market responses.

Figure 2 — Conceptual lead–lag relationship between escalation signals and market volatility

Figure 2 — Conceptual lead–lag relationship between escalation signals and market volatility. Early escalation signals may emerge before volatility indices (such as the VIX) respond, creating a detection lag for markets.

signal compression → lower signal clarity → delayed volatility response

According to reporting by Reuters and Associated Press, the most recent round of diplomatic engagement occurred during indirect U.S.–Iran negotiations in Geneva, conducted under Omani mediation, following earlier talks organized through Muscat’s diplomatic channel.

Despite those negotiations, tensions escalated rapidly. Within days of talks ending without a breakthrough, the regional environment shifted toward open confrontation, with military strikes and retaliatory actions reported across the region. These developments were widely reported by outlets including The Washington Post and Al Jazeera.

In effect, several of the traditional signals markets typically rely on to interpret geopolitical risk were either compressed or bypassed entirely.

Many hedge funds will argue that these developments are already “priced in.” In market terms, this means available information has already been incorporated into asset prices through the collective expectations of market participants.

But this raises a deeper analytical question:

Priced into what framework?

If the mechanisms through which escalation unfolds are changing—moving through compressed timelines and less formal signaling channels—then the informational environment itself may be shifting. The consensus frameworks markets use to interpret geopolitical risk may not yet be calibrated to these dynamics.

Analytical Implication

If escalation signals compress, the informational environment becomes harder for markets to interpret in real time.

In practical terms:

signal compression → lower signal clarity → delayed volatility response

This dynamic may help explain why geopolitical shocks sometimes appear to precede volatility spikes rather than coincide with them.

The muted response may therefore not reflect the absence of risk.

It may reflect uncertainty about how to price a compressed escalation environment.

Analytical note: The concept of “signal compression” refers to the shortening or bypassing of traditional escalation signaling stages. GrayStak is currently exploring methods to measure how these dynamics affect the timing of market volatility responses.

Methodological note: The concept of “signal compression” refers to the shortening or bypassing of traditional escalation signaling stages. GrayStak is currently exploring methods to operationalize this dynamic through structured event analysis and volatility response timing.